Semiconductors are the tiny chips that make modern life possible. They run our phones, cars, hospitals, factories, and defense systems. Without them, economies would stall and national security would be at risk. Beyond their strategic role, semiconductors also represent one of the fastest-growing global markets. Valued at roughly USD 681 billion in 2024, the industry is projected by the World Semiconductor Trade Statistics (WSTS) to grow to USD 701 billion in 2025. Furthermore, there is a wide consensus that revenues will surpass USD 1 trillion by 2030, a forecast supported by leading industry bodies and market analysis firms including McKinsey & Company, Deloitte, PwC, and SEMI.

Despite the enormous market value, semiconductor production remains highly concentrated and vulnerable. Advanced chipmaking demands nanometer-scale precision, specialized equipment, and investments of tens of billions of dollars. Only a handful of countries control the most critical parts of this supply chain: Taiwan and South Korea dominate manufacturing, with TSMC producing most of the world’s leading-edge chips; the United States and Israel lead in chip design; and Europe and Japan in lithography tools, materials, and other specialized equipment. This concentration leaves the world economy and national security exposed to political conflict, supply disruptions, or technological bottlenecks

These vulnerabilities have pushed semiconductors to the top of government agendas worldwide. The United States enacted the CHIPS and Science Act to strengthen domestic manufacturing and research, while the European Union’s Chips Act aims to double its global market share by 2030. Japan is subsidizing new fabs, China is investing hundreds of billions to achieve self-sufficiency, and countries from India to Israel are rolling out their own semiconductor strategies. This global race reflects both economic and strategic value in an era of geopolitical competition.

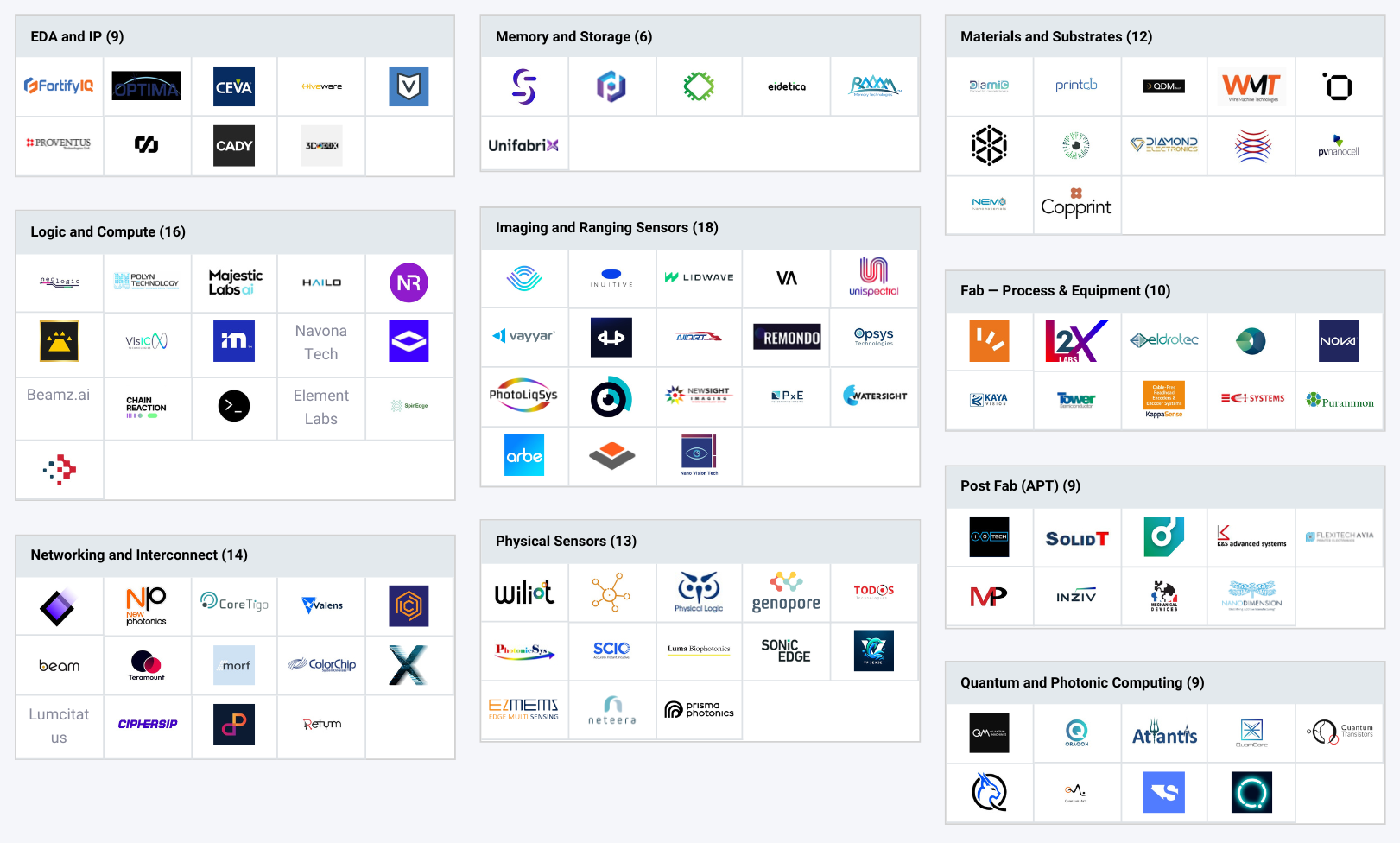

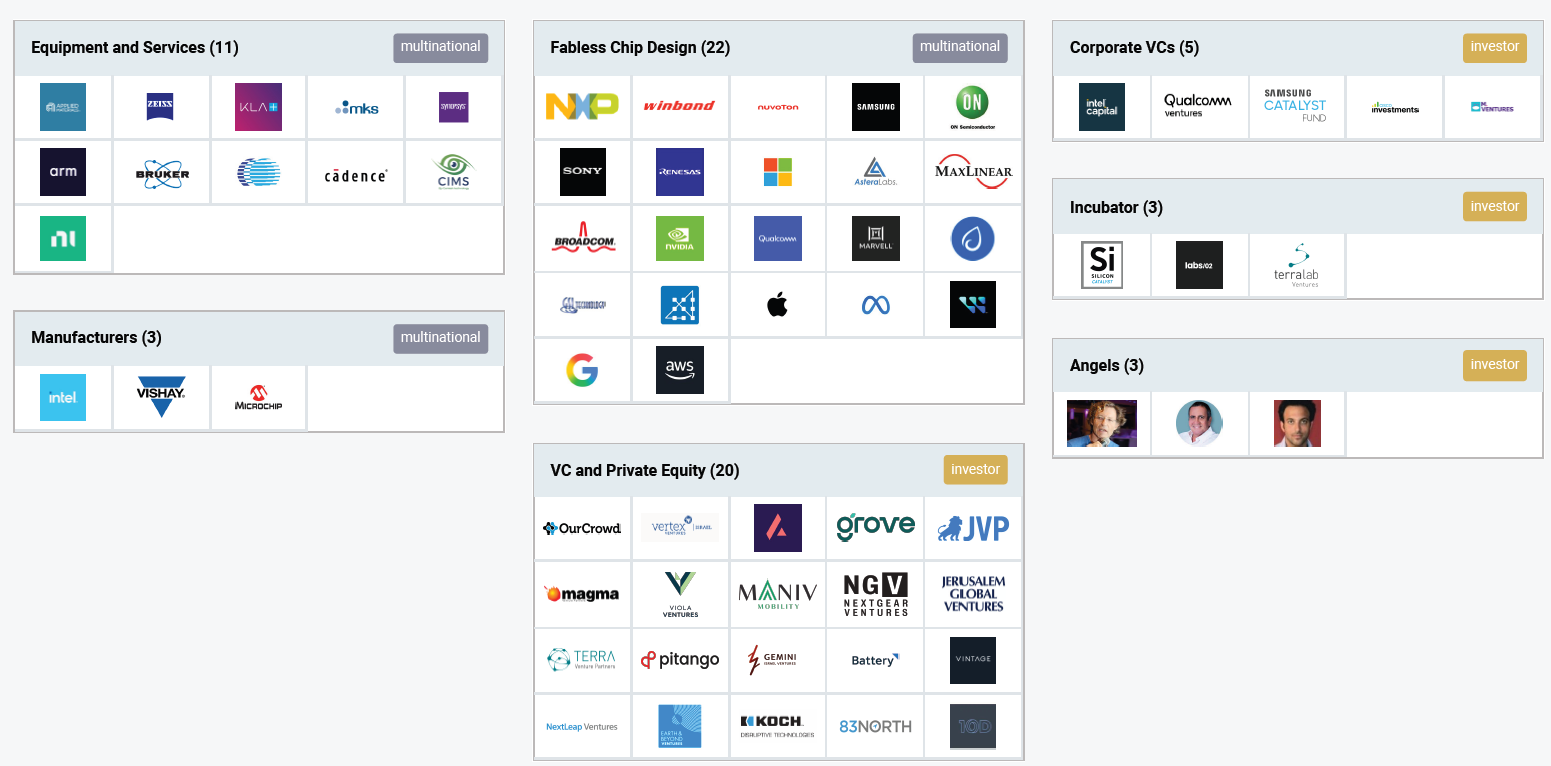

Israel is home to many of the world’s leading semiconductor companies, making it a strategic global hub. Intel operates one of its largest development centers in the country. Applied Materials runs its biggest R&D site outside the United States. Nvidia transformed its Israeli footprint through the $7 billion acquisition of Mellanox in 2020, integrating its high-performance networking capabilities—now central to AI—and becoming one of Israel’s largest technology employers, with more than 5,000 staff.

Alongside these giants, Israel’s startup ecosystem is a driving force in semiconductor innovation. Dozens of ventures are advancing AI accelerators, cybersecurity hardware, and defense-related chips, with several securing substantial global investment and scaling rapidly. This density, fueled by exceptional engineering talent, an entrepreneurial culture, and decades of strategic investment, has transformed Israel from a peripheral outpost into a global R&D powerhouse.